Navigating Shared Risks: Protecting Your Partners and Your Practice

Growth is an exciting phase for any legal practice. Moving from a solo operation to a firm of two, three, or five attorneys brings undeniable energy. You have colleagues to bounce ideas off of, the ability to take on larger, more complex cases, and the camaraderie of a shared mission. In a small firm, collaboration is your greatest strength.

However, in the world of professional liability, this closeness is also a hidden vulnerability. When you share office space, staff, files, and a letterhead, you are also sharing risk. A mistake made by your partner down the hall is no longer just their problem—it’s a direct threat to your own financial security and professional reputation.

At Professional Liability Services Inc. (PLSI), we specialize in helping small law firms navigate this critical transition. We understand the unique dynamics of a 2-5 attorney practice, from the bustling main streets of Solon, Ohio, to growing legal hubs in Georgia and Arizona. We know that a policy built for a solo practitioner is rarely sufficient for a partnership.

Here is a look at the specific risks small firms face and how the right Lawyers Professional Liability (LPL) insurance policy acts as a crucial buffer.

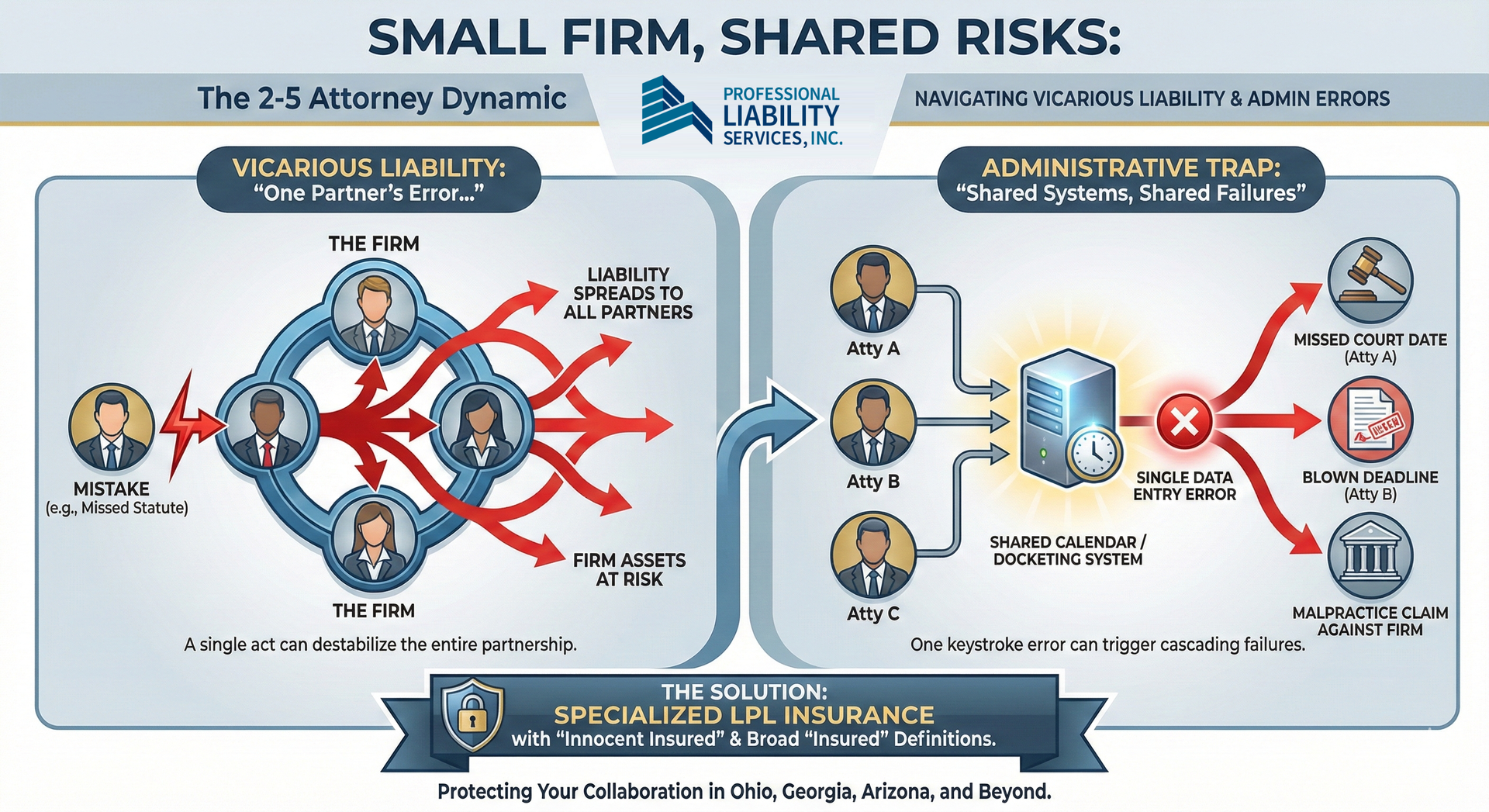

The Reality of Vicarious Liability: "All for One, and One for All"

The most significant change when moving from solo to partnership is the concept of vicarious liability. In simple terms, this means that the firm—and often its individual partners—can be held legally responsible for the negligent acts of any member of the firm, provided those acts occurred within the scope of the partnership's business.

Imagine this scenario: You are a meticulous attorney with a spotless record. Your partner, who is brilliant but notoriously disorganized, misses a critical statute of limitations filing on a large personal injury case. The client sues for malpractice. They don't just sue your partner; they sue the partnership. Because you are a partner, your firm’s assets—and potentially your personal assets, depending on your firm's legal structure—are now on the line for a mistake you didn't make.

We see this play out frequently in states like Tennessee and Kentucky, where small general practice firms are common. Without a policy explicitly designed to handle this shared liability, one partner's error can destabilize the entire firm.

The Administrative Trap: Shared Systems, Shared Failures

In a small firm, efficiency is key. You likely share paralegals, legal assistants, and a central calendaring or docketing system. While this makes financial sense, it creates a single point of failure that can have cascading effects.

Consider the shared paralegal who supports three different attorneys. A heavy workload leads to a simple data-entry error—a hearing date is entered incorrectly into the master calendar. That single keystroke error can cause a missed court appearance for one attorney, a blown deadline for another, and a malpractice claim against the firm based purely on administrative negligence.

When we review insurance applications for small firms, we look closely at their risk management procedures. But even the best systems can fail due to human error. Your LPL policy needs to be the ultimate backstop for these inevitable administrative slip-ups.

The Critical Importance of the "Innocent Insured" Clause

What happens in a worst-case scenario? Let's say a partner at your firm misappropriates client funds or commits a fraudulent act. Insurance policies generally exclude coverage for intentional, criminal, or fraudulent acts. A carrier might argue that because one partner committed fraud, the entire policy is void, leaving the remaining, honest partners without any defense coverage.

This is where an "Innocent Insured" provision becomes a financial lifesaver. This clause ensures that the policy will still provide coverage for the "innocent" partners who had no knowledge of or participation in the wrongdoing. They are protected from the fallout of their partner's bad acts. For any partnership, this endorsement is not a luxury; it is an absolute necessity.

Defining "The Insured": Closing Coverage Gaps

Small firms often have fluid staffing models. You might have equity partners, non-equity associates, an "Of Counsel" attorney who comes in for specific cases, or contract lawyers hired for temporary help.

A generic, off-the-shelf LPL policy might have a very narrow definition of who qualifies as an "insured." If a contract lawyer working on your firm's behalf makes a mistake, and the policy’s definition of "insured" doesn't explicitly include temporary or contract staff, the carrier could deny the claim.

At PLSI, we meticulously review the "Definition of Insured" section of every policy we recommend. We ensure that the language is broad enough to cover every individual acting on behalf of your firm—from the senior partner to the part-time paralegal.

The PLSI Advantage for Small Firms

You wouldn't ask a general practitioner to perform heart surgery. So why trust the financial heart of your firm to a general insurance agent who mostly sells auto and home policies?

Professional Liability Services Inc. is highly specialized. LPL insurance is all we do. We have decades of experience navigating the specific policy forms, exclusions, and endorsements that matter most to small law firms. We work with over 20 top-rated insurance carriers to find a policy that is tailored to your firm's specific size, practice areas, and jurisdictional risks across our licensed states of Ohio, Michigan, Indiana, Kentucky, South Carolina, Tennessee, Arizona, and Georgia.

Moving from a solo practice to a small firm is a sign of success. Don't let the hidden risks of growth undermine what you've built. Let us help you put the right protection in place so you can focus on collaborating with your team and serving your clients with confidence.